India's Not-So-Mythical Unicorns 🦄 (Part I)

Mere desh ki dharti sona ugale, ugale heere moti aur unicorns

VC Uncle: Beta bade hokar kya banoge?

Mom: Mera beta engineer banega

Dad: Mera beta doctor banega

Startup Beta: Uncle mai Unicorn banunga 😎

Unicorn - *dramatic drum beats* - the buzzword of the VC space and the glorified dream of many a yearning startup. This badge of honour has been the make or break point for some while a non-consequential feather in the hat for some, but what it undeniably is, is a free ticket to fame and recognition.

While unicorns have been a creature of fables and legends, they are not so ancient in the startup world. The term was coined only in 2013 to describe privately held entrepreneurial ventures that were valued at $1 billion.

From 39 in 2013 to 491 as of this week, these billion-dollar (and more) valued startups are multiplying like crazy as industries mature. The United States, no surprise, leads the population at 223 unicorn startups, followed by China at 118 unicorn startups.

In India, the unicorn story has been slow but it is definitely picking up pace. At present we have somewhere around 23 unicorn startups.

This got us thinking -

Which was the first unicorn startup in India? 🧐

Records suggest it was Bangalore-based (not even surprised there) marketing-tech startup InMobi, which began operations in 2007.

Since we are *Fintech* Femme, our obvious next question was -

Which was the first fintech unicorn, then? 🤔

We'll give you some space so you can play this game with us. Guess karo, and then scroll below to find the answer 👀

🦄

🦄

🦄

🦄

🦄

🦄

🦄

🦄

🦄

🦄

🦄

🦄

🦄

🦄

If you guessed Paytm, you are absolutely right! 🥳

Indian fintech ki shaan and Vijay Shekhar Sharma ki maan. 🙌🏼

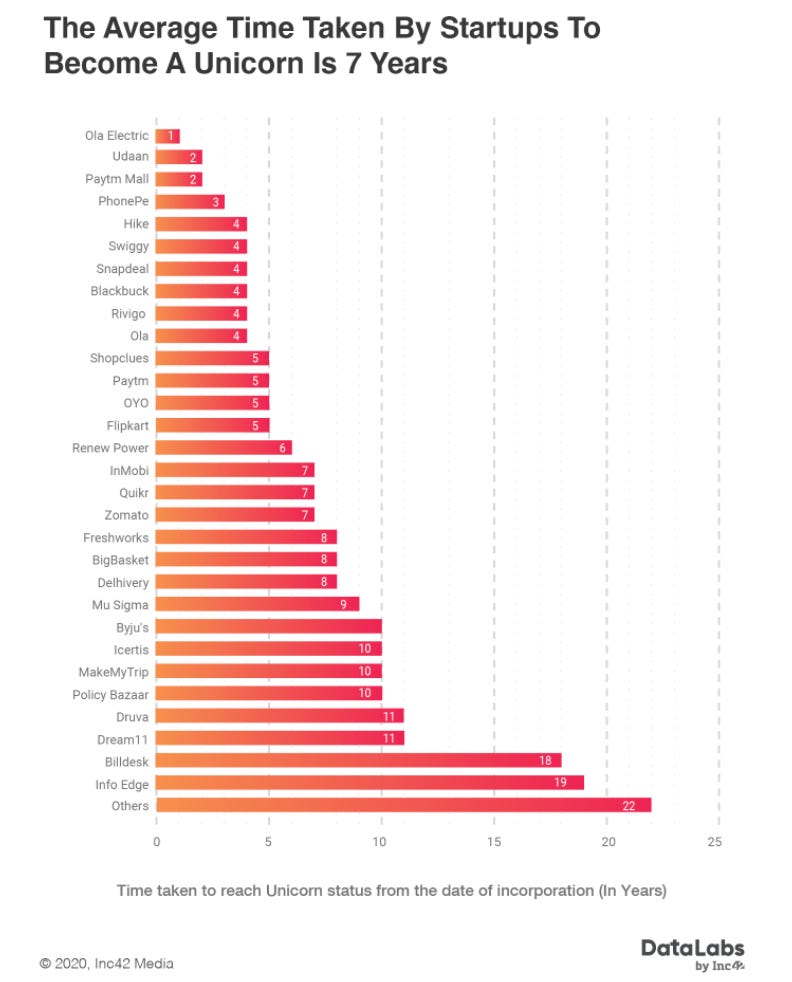

Time to unicorn (TTU), the time taken from inception to the point of attaining billion-dollar valuation by a startup, is an interesting indicator of the maturity of a particular region's startup ecosystem. Time taken to reach unicorn valuation for Indian startups is shrinking drastically as startups' use of technology advances. In India, the metric is currently at 7 years, while it's at 6.5 years in USA and 5.5 years in China.

This (not so) little infographic by Inc42 gives a good birdseye view to Indian startups' TTU:

Moving onto our bread and butter - fintech startups.

On a global scale, fintechs take an average of 7.15 years to reach unicorn valuation, while interestingly the median for the same sample set is 5.33.

The Indian fintech segment in particular, which has around 8 unicorns, the TTU is about 10.4 years.

Enough of stats for this blog. It's storytime, kids! Let's have a look at India's fintech unicorns, their uphill journeys and what it took for them to get the Scouts' badge of Unicorn.

Pine Labs: Graduated Gradually

Time to unicorn: 22 years

To all the 2020 post-graduates out there, if you feel you’re the only one who can’t celebrate the 22 years of hard work with a perfect moment, we’ve got something for you!

Say hello to the 22-year-old startup who finally made it to the Unicorn list in 2020 - Pine Labs.

(We’re in this together, reaching new highs amidst a pandemic 🙂)

You’ve probably seen the two green pine leaves every time you’ve made a payment at any major chain restaurant or shopping place - online or offline.

With that kind of market existence, what took Pine Labs 22 years to make it to the Unicorn list?

Let's go back to where we started. Consider Pine Labs growth story like a 22-year-old kid who struggled in school days, managed to get into a decent college and with consistently good performance, a straight-up entry to one of the prestigious IIXs and boom - flying colours? Na. more like a flying horse!

This kid started in 1998 with just a petro-card business and continued forming a stronger base out there till 2004, where they entered petro-focused POS solutions. Meanwhile, one of the founders had left the organization.

Fast forward to 2009 where they raised seed capital from Sequoia, simultaneously taking baby steps to their real payments journey by connecting merchants and banks. By this time, the second founder left the organisation too.

2/3rds of the non-existent founding team is talk of extreme demise for any company but this visionary kid decided to continue on a single pillar.

With one co-founder still standing strong as a CEO - 14 years later like any other kid who’s excited to enter a new college, Pine Labs took a first big step towards a renewed journey of cloud-based POS systems.

Since then with every passing year, they kept evolving with the turn of events happening around. RBI announced TLE mandate (4 digit pin) in 2013 which helped Pine Lab’s POS demand reach new highs. Next?

Well, with the existing fame the helped make merchants learn new things about their friends (customers) by giving them access to real-time sales data, moving on with loyalty programs, enabling UPI and wallet-friendly POS and finally ending 5 years of graduation by a bang on launch of the “data-mining” business...Lending!

Inspired by any other Indian, Pine Labs went international after the graduation and partnered with CIMB Bank. In the next two years, they raised $82Mn from Actis and Altimeter Capital followed by Temasek and PayPal’s minority stake at $125 combined!

Enter 2020: Pine Labs finally became a unicorn post their recent round of investment via Mastercard! *insert slow claps*👏

Currently, they have 150K+ merchant relationships over 3700+ cities with a little change in leadership positions. Amrish Rau, the man biggest Indian Fintech deal of India is now the CEO of Pine Labs. If the company grew with one strong co-founder at initial stages, we can only imagine the wonders this man can bring about!

BillDesk: Up For Sale (Again)

Time to unicorn: 18.8 years

Another oldie but goodie from the payments space, Billdesk has been in the news recently and previously for talks of getting acquired. That ship hasn't sailed yet, but it might very soon. Valued at $2.5 billion dollars, what makes this unicorn so elusive to potential takeovers?

Established in 2000, Billdesk was at the forefront of ushering in the digital payments era. As the years passed and the adoption of digital payments kept growing with debit & credit cards, bank transfers, e-commerce, e-wallets and e-everything, payment gateways emerged to be a vital piece of the backend puzzle.

Although competition is high coming in from all fronts with youngbloods like RazorPay, PayU, NPCI's Bharat Bill Pay System & even firangi Stripe showing interest in Indian markets, Billdesk has a nice moat set up for itself. It processes $80 billion per year and enjoys a solid 50% market share in bill payments - rightly so given its vintage. The company took the smart path to viability by becoming an enabler to the bigger fish in the sea, rather than going head to head with the sharks (read banks). It counts a majority of Indian banks and utility providers as its clients and even e-commerce giants like Amazon India.

While the recent happenings in the payments space have been not so friendly towards payments service providers, Billdesk is doing pretty well for itself remaining profitable throughout. Also, a promising signal was a 77% drop in expenses from FY17 to FY18 combined with a conservative 15% rise in profit during the same period. It was during the same time that the payments fintech sprouted its magical horn and bagged $75 million from Visa, valuing it at $1.8 billion - a straight-up 3x jump from its previous valuation at $584 million. Also, to note that this was Visa's very first investment in India. Given the rise of UPI & RuPay, it was a logical move for the payments giant to strengthen its hold in the country.

Talking about the matter of putting the business up for sale - the rising competition in the payments space seems to be the primary driver. Its previous attempt at selling a partial stake didn't get any takers sadly. Now, the fintech is making a smarter move of quitting while it's ahead, instead of succumbing to its own death - and we really respect that. 20 years is no small feat, and the company that does end up acquiring BillDesk will be getting nothing lesser than an infinity stone on its payments gauntlet. 💎

Policy Bazaar: Ek Saal Mein Growth Double!

Time to unicorn: 10.9 years

Back in the crisis-affected year of 2008, two individuals who used to work in a global insurance broking company called First Europa decided to create a platform where Indians visit to just compare their options of insurance policies.

But wait, what about that guy who told me “Madam, this is the best for you.”?

This thought certainly wasn’t random. Lack of financial knowledge in India is something that we aren’t very proud of, and insurance being one of the most complex products had a HUGE ratio of mis-selling. Most of the people won’t have an answer as to why they have bought a particular policy in the first place. Insurance is a product for those who cannot afford medical expenses and let me shift your focus on this “Ironic moment 101” - according to a 2019 survey, 90% of the poorest Indians do not have health insurance.

Here’s when policy bazaar thought of aggregating the insurance policies on one platform for better comparison and moreover, not trusting that one guy who randomly rings your doorbell expecting that you’d trust him with something as serious as your life.

Take a pause here and try to imagine the revolutionary quality of this thought back in 2008.

Now the question here is what took policy bazaar 12 years to get that magnificent horn on their existing horse-like business model, despite being the first movers in aggregation of financial products as a concept?

In our opinion, unlike most startups who aim for preparing the fully loaded Rajasthani thali on their table, policy bazaar concentrated on making their piece of rice better by just spicin’ it up a lil’ every now and then.😉

The company proudly boasts about growing over 100% YoY since inception! They sell 400K policies every month and currently account for 25% of India’s life cover. Let’s give these guys some cookies for swooping away 50% of the online insurance market even with the newbies coming in and selling small insurance products you can buy for 1 rupee before taking your Uber. Yep, sixes over twos, that’s how you win the match.

Speaking of cricket, a quick fun fact in IPL season:

Eden Gardens in Kolkata is the biggest stadium with a seating capacity of 68,000 humans. Now make your brains go wild and imagine the people in here, multiply it by 4 and that’s the number of people who visit policy bazaar in a day!

These numbers are enough to tell you that even with a single-digit lead generation rate, policy bazaar manages to gain a substantial amount of money for charging around 60 rupees per lead! And oh, don’t forget the content-led marketing.

So here’s to the unicorn who religiously kept focusing on the core traditional business, slowly moving from just a lead-generation platform to now providing end-to-end service for buying insurance, but nothing more. They are now shifting focus on the above-mentioned untapped health insurance market and sure as eggs have a huge market to capture!

Also, watch out for the rumour-mongered IPO plans in 2021!

Paytm: Currently Resolving Cashback Wars

Time to unicorn: 5.3 years

Maano ya na maano, Paytm holds a special place in every Indian fintech nerd's heart. The first fintech unicorn of India and there couldn't have been a better one honestly. The financial superstar that Paytm is today, is nothing short of a humongous feat to achieve in 10 years since inception. $16 billion in valuation, $4.4 billion funds raised, Rs 3,232 crore in revenue, but Rs 4217 crore in losses. *slowly closes door*

*another door opens* But hey, the company is apparently pretty confident on its path to profitability by 2022. How so you may ask? Well, if you zoom out to see the bigger picture of Paytm, apart from payments which form 56% of its revenues, they are a bookings aggregator, they are a payments bank, they are an AMC, also a stockbroker, and they also acquired a general insurance company recently.

The ultimate road to profitability lies in diversifying a building stable revenue streams and that's what Paytm has been doing all this time putting all these blocks into place. Not gonna lie, they've burnt some serious cash to remain where they are (talk about marketing spend exceeding revenue - BRUH 🤯), but there is a fairly optimistic chance this helps them build customer stickiness and eventually increase the multiplying value derived in return over time.

As for its unicorn status, the badge actually belongs to its parent entity One97 which has a dated history. What made One97 a unicorn was the wild success of Paytm. The small little e-wallet that was launched in 2010 mainly for mobile recharges, grew leaps and bounds. Between 2014 and 2015, the user base went from 11.8Mn to 104Mn and with UPI coming into the picture in 2016, it added another tailwind to the gliding ship.

Also not to be overlooked its the powerful (and slightly controversial?) investors the company bagged over the years - Tencent, Softbank, Alibaba - you name it! Everyone wanted a piece of Indian fintech's golden egg and so the valuations continued to soar.

The path ahead is still a challenging one for the payments rockstar, with its core focus on profitability. With the charisma and strong leadership of Vijay Shekhar Sharma, the company seems to be in able hands to overcome all the unseen hurdles.

Udaan: Hum Toh Udd Gaye, Udd Gaye

Time to unicorn: 2.7 years

Ola Electric may have zapped up to unicorn valuation in a year, but Udaan's rocketship wasn't far behind. The fastest among the fintechs to gain the coveted billion-dollar pin, Udaan which was established in 2016, turned unicorn in September 2018 with its Series D funding from DST Global & Lightspeed India Partners.

You may think Udaan is a B2B marketplace, where's the fintech? Well, very similar to their origin story for building a product for the backend market of manufacturers & wholesalers, Udaan's backend business model is pure fintech at heart. While the marketplace acts as a means to engage and onboard customers, the transactions taking place on it help the startup earn commission income. Customer retention also happens through working capital loans which are the lifeblood of small businesses. This essentially helps the startup build a robust loan book and an inflow of a steady revenue stream from interest.

While the exponential growth witnessed by the fintech has been nothing less of a whirlwind dream, it does come at a cost. Cash burn is a Pandora's box that too many startups have fallen victim of. Udaan's burn rate to capture the B2B space has been pretty high - it spent about $15 million in 2019 on the task. This might sound a bit concerning but once you get to know the possible influence of this trait you might just laugh it off as 'hah, so typical'.

Udaan was the brainchild of 3 ex-Flipkart employees - Amod Malviya, Sujeet Kumar and Vaibhav Gupta. As we all know, e-commerce giants have had quite a flair for cash burn, so this characteristic of the fintech doesn't seem too out of place. However, cash burn wasn't the only thing the founders picked up. Flipkart being the e-commerce heavyweight that it is is a ripe playground for invaluable learnings and boy has it shaped the founders to reach where they are today.

Self-valued at $7.5 billion based on its projected cash flows and equity infusions, the fintech has mapped out a clear path to profitability by 2022. This is the kind of confidence we like and with the way the company has been blazing through, it seems investor confidence is high as well. Udaan's mission to the unicorn Moon was a successful one, but perhaps there are bigger things on the horizon and decacorn Mars is the next destination? 🚀

These final two fintechs we have next are kind of the Chupa Rustam Unicorns. While they don't get considered in official counts of Indian fintechs in many global publications, they are very much unicorn in DNA and in valuation.

PhonePe: The Fintech With Some Wealthy Sugar Daddies

Time to unicorn: 3.2 years

PhonePe enjoys a lot of perks thanks to Flipkart and Walmart. Its funding and valuations are definitely a few of those. 4 funding rounds in 2019, 2 in 2020 already - thing to be noted is that Flipkart is the only investor, matlab pappa ka hi paisa hai.

The acquisition by Flipkart happened even before the product went live. The company was started by 3 ex-Flipkart peeps in 2014 as FxMart. The idea for PhonePe came later on as UPI was launched in April 2016. Flipkart, looking to reserve its piece of the payments cake, quickly bought PhonePe to operate as an independent unit under the group company.

When PhonePe launched in August 2016, it rode the UPI wave like a pro with a multiplying user base and market share. Within 3 months of launch, the app was downloaded by more than 10 million users. By August 2017, it had taken over BHIM UPI in market share. At the time, PhonePe & BHIM governed 87% of UPI transactions, with no Google Pay in the picture yet.

In 2018, Walmart took interest in India and took up a controlling stake in Flipkart - tum sher ho toh hum sawa sher! The smart move through all of this has been keeping PhonePe as an independent entity. This has helped the company establish its own persona as well as giving it the freedom to pursue external funding, which had some talk going around the VC town in 2019 of PhonePe looking to raise $1 billion from A-listers like Tencent & Tiger Global. The most ambitious of it all is the company's plan to go public by 2023 at a valuation of 8 to 10 billion dollars.

PhonePe is brilliantly proving that it's not a one-trick-pony. Expansion into segments like wealth management with mutual funds and insurance has shown positive results for the company. During the nationwide lockdown, the fintech managed to sell over 500,000 insurance policies to its tier 2 and tier 3 concentrated user base. An amazing feat given its nascency in the segment.

The fintech's valuation is a bit of a T&C applied situation given its ownership. It achieved unicorn status in February 2019 and its last funding round in December 2019 valued it at $1.9 billion. In September 2019 Morgan Stanley had valued the company at $7 billion in a base case scenario (again, lots of T&C applied). In FY19, the fintech spent Rs 2153 crore to earn a mere Rs 184 crore in operating revenue, while its losses increased 2.4x to Rs.1907 crore. It's also reported having a monthly burn rate of $15 million which is hot hot hot! No wonder Flipkart keeps pumping in so much money - $928 million to date if you're counting.

The tunnel vision for PhonePe right now is aimed at profitability as soon as 2022, as is the case for most fintechs. The UPI champ may have some fluffy back-up cushions and pockets to fall back on, but we guess it's time they prove themselves to be capable of standing up on their own.

Zerodha: Zero Se Hero

Time to unicorn: 10 years

Popcorn is highly recommended for this one.

Ever been to a sale? All of us are so used to seeing the small asterisk mark saying “*T&C apply”

Quite evidently, it was quite overwhelming to believe when Zerodha launched claiming zero brokerages and flat 20 rupees for intraday and F&O trades. The brains of folks in our own “Satta bazaar” assume that everything that’s available for cheap is a scheme.

Well, not this time. Zerodha was probably the game-changer and boss of what we now term as “discount broking”.

The idea of any kind of discount is to attract more audience and earn by the multiplying effect of buyers. However, the ambiguity of this situation was India does not have a whole lot of active traders, to start with. For attracting the existing ones, it would demand lots of effort for them to even start trusting you as an actual company.

Enter: Nithin Kamath, the hero of this story who formed Zerodha with the aim of making investing easier with the help of technology...without knowing anything about technology. One of his interviews mentioned: the only tech he knew was excel. This, with the help of his brother Nikhil Kamath, the brains behind the trades.

Enter: Kailash Nadh, the supporting actor who helped build the tech, well you guessed it - without knowing finance. Oh now that love story already deserves the unicorn badge but, there’s a lot more to this.

Although Zerodha started with a simple aim of “making it simple”, it ended up doing something huge in these 10 years. Not only is the company profitable since the very first year, they are legit trying to build a whole community including every tiny detail of the financial markets. Now’s the right time to grab some popcorn, *drama alert!*

With the smashing “discount broker” launch, the market legit speculated their authenticity, and forming the first base of the community must’ve surely been difficult for them. Thanks to the community blog z-connect which helped Zerodha gain a fairly confident audience on the platform. Fixed.

Enter: Bad guy #1.

The ambiguous situation we mentioned above, what about the lack of financial knowledge in Indians without which it would be difficult for Zerodha’s model to work.

Launch: Varsity in 2014: a learning platform for a naive to understand the stock market. Fixed.

Enter: Bad guy #2.

Who hasn’t heard about the classic “technical glitch” on Zerodha platforms due to high frequency of trades? The frustration stop losses of their customers were certainly triggered, if not the actual ones.

Launch: Kite in 2015, the flagship platform which Zerodha claims to be ultra-fast. Fixed? We’ll let the users decide on this one.

Enter: Bad guy #3.

So we’re doing pretty good on gaining traction to trade equities in markets but is that really enough? What about the “Sahi hai” asset class?

Launch: Coin in 2017, the commission-free demat delivered online mutual fund platform. Fixed.

Enter: Bad guy #4.

By 2018. Zerodha was the talk of the town. Users kept multiplying. What more can we do to keep them even more engaged and probably try to analyze data and what stocks are they engaging with?

Launch: Sentinel in 2018, A stock monitor to create alerts that stay on the cloud for years. Fixed!

Enter: Bad guy # 5.

Hey, look! We probably put our users in a “juggling app” situation after these launches. Where would one focus while making a trade? The main app? Kite? Sentinel? What was the name of that mutual fund app, again?

Launch: Console in 2019. A central Dashboard for your Zerodha account. Fixed.

Okay, we’ll stop with the bad guys count because now we have an army of 20, like in a Rohit Shetty movie. What about the other pieces like fixed income, algo trading, long-term investments and also micro-savings investments?

Nevermind, this time we get a superhero!

Launch: Rainmatter. Literally, a whole new incubator to invest in all possible players of the ecosystem. FIXED!

Zerodha now has over 3 Million users and has paved its way to becoming the largest broking house of India, overtaking traditional players like ICICI Direct and HDFC Securities. It has strategic investments in small companies like Smallcase, Streak, Sensibull, Finception, GoldenPi and many more!

Indeed a well-deserved unicorn. Did I stutter?!

Boy, has this has been a loooong post, eh? We just couldn't help ourselves when we got to writing about these fintech darlings of India. 🥰

To keep you hooked, the next instalment of this post will be about the soon-to-be-unicorns where we predict the next entrants to the fintech unicorn club. So we hope you prepare your predictions for the upcoming part II because it's surely going to be an entertaining and exciting one! 🤩

References for funding & valuation from CB Insights & Crunchbase. Company-specific details from publicly available sources such as press releases and news outlets.